Discipline before cleverness.

Burned by Intuition

Actuaries are clever people, and work with other clever people, and together they can all model lots of things intuitively. For example, an actuary might have two models with different data or methods trying to estimate the same phenomenon. Under model X they get an estimate of 5%, and under model Y they get an estimate of 8% (They're actuaries, so it's likely an Excel spreadsheet and only point estimates, sadly). However, the actuary trusts the data in model X more than in Y, so they use their actuarial judgment, hunch, best guess, industry knowledge, prior, or intuition to weight X and Y by 80%/20% to get a combined X/Y result of 5.6%.

But intuition can fail us. Consider this Richard McElreath variation on the Monty Hall problem:

Someone is cooking pancakes. They have to calibrate the stove temperature, and as a result, the first three pancakes come out like this:

- Burned on both sides

- Burned on one side, perfect on the other

- Perfect on both sides

You are served a pancake, and you only know the top side is burned. What is the probability that the other side is also burnt?

The common intuition is that you must have one of the two pancakes with a burnt side, so 1/2. But this is wrong.

To reason about this correctly, you need formal probability theory. Thus, let me formally introduce you to Bayes' theorem.

Bayes' Theorem

Bayes' theorem is a framework for updating our beliefs in light of new evidence. In this framework, probability is the numeric assignment of belief in something.

The denominator

This ensures that the posterior probability

Returning to the pancakes (which, unfortunately, are cold now), we can use Bayes' theorem to calculate the probability that the bottom side is also burnt, given we see the top side is burnt.

Next, we compute the total probability of observing the evidence

Now substitute the values:

Substitute the values:

There's a 2/3 chance of having the burnt pancake on both sides; not 1/2. It's not intuitive.

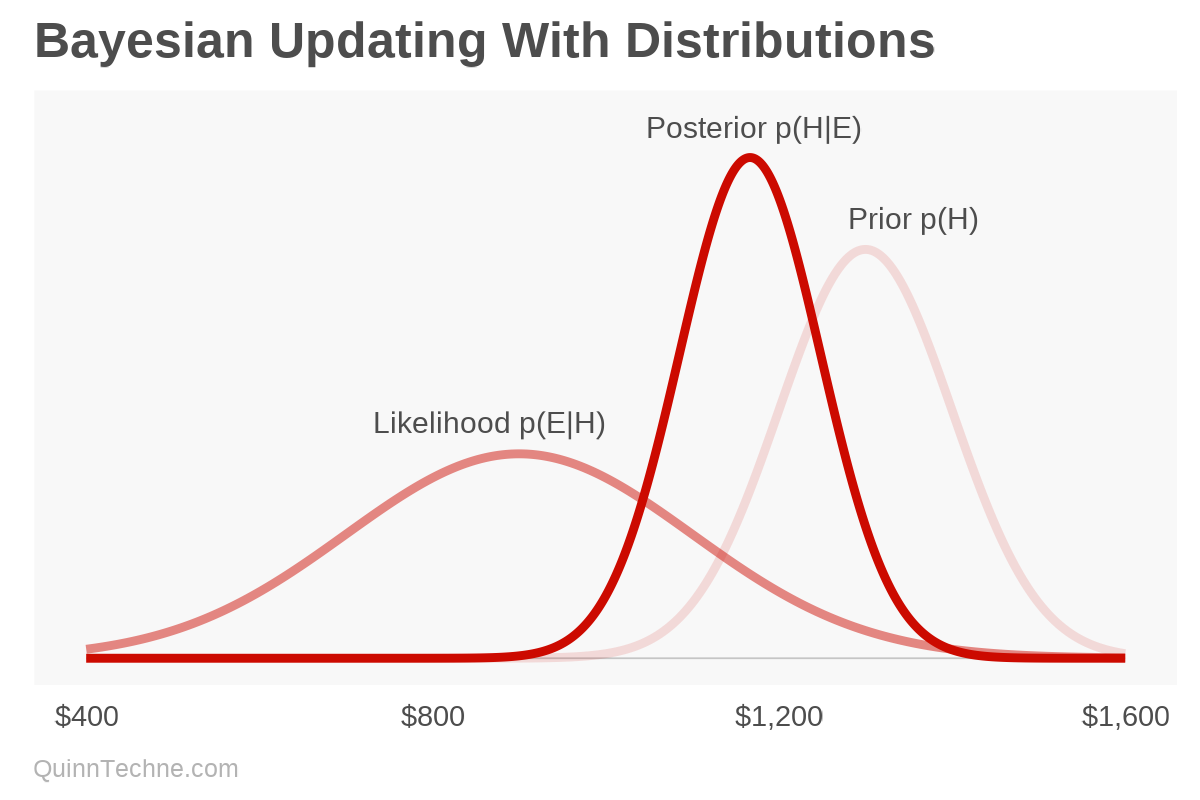

The Full Enchilada

Here's another example showing how Bayesian inference can extend from point estimates to distributions. But first, a simplified Bayes' theorem:

This form may appear different from the previous version, and the symbol

How does it work? Suppose an analyst is forecasting the annual cost of something. They assume it is normally distributed (Gaussian or bell-shaped) with a mean of $1,300 and a standard deviation of ±$100. This is their prior.

The analyst then gets two data points: quarterly costs. They assume these costs also come from a normal distribution. After annualizing the costs and adjusting for inflation to the forecast period, the analyst has $950 and $850, believing they have a standard deviation of ±$200. You encode your uncertainty in the variance, precision, volatility, spread, or standard deviation. The analyst is less certain from a quarter's worth of data versus an annual forecast—think Central-limit theorem and the square root relationship of standard deviation to sample size.

- Prior: Normal($1,300, ±$100)

- Likelihood: Normal(E, ±$200)

- E, evidence, or new data: $950, $850

- Posterior: wait for it...

- Posterior: Normal($1,167, ±$82)

We started with our prior of $1,300 and have a new average of $1,166 after seeing the new data. Bayesian updating, ta-da!

Calculating Posteriors

So, how can one calculate these? Here are a few examples in R. Setting up these R methods usially requires free software besides R, like Rtools, Stan, or JAGS. We are going to use the same numbers as the chart, which means we're updating our prior, the mean, which is called mu (μ). First, we'll look at quap(), which approximates the posterior distribution, making it very fast. It is part of the rethinking package, and the example shows the slim version which requires no extra software. Then we'll look at rjags and cmdstanr which use a simulation method called Markov chain Monte Carlo (write that down, it'll be on quiz at the end). Last, we'll show brms which is also Stan, but written like a vanilla R regression model.

quap

# Install quap()

# install.packages(c("coda","mvtnorm","devtools","loo","dagitty"))

# devtools::install_github("rmcelreath/rethinking@slim")

library(rethinking)

# Model

flist <- alist(

new_data ~ dnorm(mu, 200), # Likelihood with known standard deviation

mu ~ dnorm(1300, 100) # Prior

)

new_data <- data.frame(new_data = c(950, 850))

# Fit the model

mod_quap <- quap(flist, data = new_data) > precis(mod_quap) # Posterior distribution

mean sd 5.5% 94.5%

mu 1166.67 81.65 1036.17 1297.16JAGS

library(rjags)

# Model

# Note that the syntax uses precision (1/sigma^2) instead of variance (sigma^2)

model_string <- "

model {

for (i in 1:N) {

new_data[i] ~ dnorm(mu, 1/(sigma^2))

}

mu ~ dnorm(1300, 1/(100^2))

sigma <- 200

}

"

data_jags <- list(new_data = c(950, 850), N = 2)

# Fit model

model_jags <- jags.model(

textConnection(model_string),

data = data_jags,

n.chains = 4,

n.adapt = 500

)

parameters <- c("mu")

# Sample posterior

samples_jags <- coda.samples(

model_jags,

variable.names = parameters,

n.iter = 4000

)

> summary(samples_jags) # Posterior distribution

Iterations = 1:4000

Thinning interval = 1

Number of chains = 4

Sample size per chain = 4000

1. Empirical mean and standard deviation for each variable,

plus standard error of the mean:

Mean SD Naive SE

1167.1296 82.2417 0.6502

Time-series SE

0.6502

2. Quantiles for each variable:

2.5% 25% 50% 75% 97.5%

1007 1111 1168 1222 1327

Stan

# Loading Stan

library(cmdstanr)

cmdstan_path()

cmdstanr::check_cmdstan_toolchain(fix = TRUE)

set_cmdstan_path(path = 'c:\\cmdstanr\\cmdstan-2.35.0') # System dependent

options(

mc.cores = parallel::detectCores(),

stanc.allow_optimizations = TRUE,

stanc.auto_format = TRUE

)

# Model

code_stan <- write_stan_file(

"data {

int <lower=0> N;

array [N] real new_data; //Object, size, variable type, variable name

}

parameters {

real mu;

}

model {

mu ~ normal(1300, 100); // Prior

new_data ~ normal(mu, 200); // Likelihood

}"

)

# Compile model

mod_check <- cmdstan_model(code_stan, compile = FALSE)

mod_check$check_syntax()

mod <- cmdstan_model(code_stan, pedantic = TRUE, dir = 'c:\\cmdstanr')

data_stan <- list(N = 2, new_data = c(950, 850))

# Fit and sample

fit <- mod$sample(

data = data_stan,

iter_warmup = 200,

iter_sampling = 4000,

chains = 4

) > fit$print() # Posterior distributions

variable mean median sd mad q5 q95 rhat ess_bulk ess_tail

lp__ -3.24 -2.95 0.74 0.31 -4.73 -2.73 1.00 7283 8344

mu 1167.49 1167.50 82.52 80.95 1031.28 1305.12 1.00 5715 7700brms

library(brms)

new_data <- c(950, 850)

# Create a formula that uses the known standard deviation

brms_formula <- bf(new_data ~ 1, sigma = 200) # Likelihood

# brms model

mod_brms <- brm(

formula = brms_formula,

data = data.frame(new_data = new_data),

family = gaussian(),

prior = c(

prior(normal(1300, 100), class = "Intercept") # Prior

),

chains = 4,

iter = 4000,

warmup = 200

)> summary(mod_brms)

Family: gaussian

Links: mu = identity; sigma = identity

Formula: new_data ~ 1

sigma = 200

Data: data.frame(new_data = new_data) (Number of observations: 2)

Draws: 4 chains, each with iter = 4000; warmup = 200; thin = 1;

total post-warmup draws = 15200

Regression Coefficients:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

Intercept 1166.59 82.95 1000.78 1326.43 1.00 6013 7822

Further Distributional Parameters:

Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

sigma 200.00 0.00 200.00 200.00 NA NA NAThis is a simple Bayesian model calculated four different ways. In all cases, the posterior distribution of mu, the updated mu given the data, is around 1,166. Yet, this simplicity can easily extend into powerful regression and time series models. These more complex models come with comprehensive workflows, model diagnostic, and best practices, but we'll save those for another day.

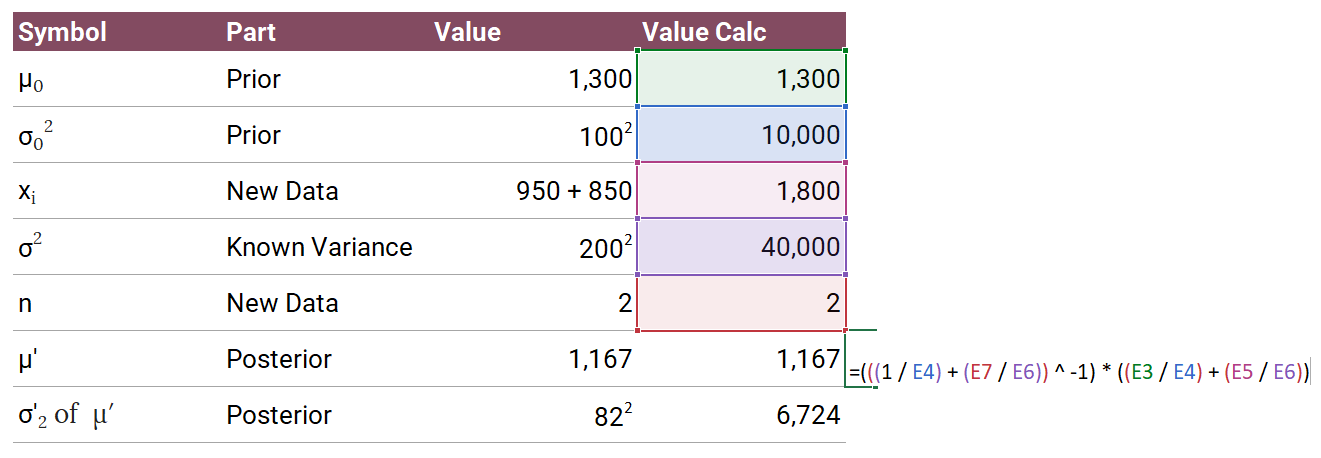

Because, Excel

Wait! I'm only comfortable with Excel. Please, please show me how to do this in Excel! Okay, fine. But you didn't learn this from me.

You can algebraically solve some types of posteriors. This example we're using is a known variance case, so you can use a normal-normal conjugate update. We'll use the formulation from Wikipedia.

The posterior update for

- Prior:

- Posterior: Updated

The posterior update formula is:

Where:

Here's how it comes together.

And how does this posterior average compare to other results?

| Package, Function | Posterior Average |

|---|---|

| Rethinking, quap | 1,166.67 |

| JAGS, rjags | 1,167.13 |

| Stan, cmdstanr | 1,167.49 |

| Stan, brms | 1,166.59 |

| Excel | 1,166.67 |

Weighty Jargon

Communicating Bayesian concepts can be confusing for most audiences. But, if your credibility is ever in a pinch, just say "posterior predictive distribution," and like abracadabra! you're credible again. Or, you can also compute an implied weighting between your original (prior) value, new data, and result (posterior) and communicate that instead. For example:

Weight on prior data: 66.6% (It's just coincidence—you wanted the dark arts!)

The implied weight is a function of our uncertainty encoded in our prior or likelihood. In this example, only the Likelihood changes. A smaller standard deviation means you trust the new evidence more and more weight would be given to the new data. A larger standard deviation means more uncertainty and thus less weight on the new evidence. This relation goes for the standard deviation on your prior, too.

Encoding Intuitions

Bayesian models offer an intentional and transparent way to update our forecasts based on new data. So, when it's time to integrate new evidence (or send your pancake back to the chef), consider making the formal calculation—your conclusions will be all the more disciplined for it.

McElreath, R. (2020). Statistical Rethinking: A Bayesian Course with Examples in R and Stan (2nd edition). Chapman and Hall/CRC. https://xcelab.net/rm/

Wikipedia contributors. (2024). Conjugate prior. In Wikipedia, The Free Encyclopedia. https://en.wikipedia.org/wiki/Conjugate_prior

Calculations and graphics done in R version 4.3.3, with these packages:

Chang W, Cheng J, Allaire JJ, Sievert C, Schloerke B, Xie Y, Allen J, McPherson J, Dipert A, Borges B (2024). shiny: Web Application Framework for R. R package version 1.9.1. https://CRAN.R-project.org/package=shiny

McElreath R (2024). rethinking: Statistical Rethinking book package. R package version 2.40. https://github.com/rmcelreath/rethinking

Plummer M, Stukalov A, Denwood M (2024). rjags: Bayesian Graphical Models using MCMC. R package version 4-16. https://CRAN.R-project.org/package=rjags

Qiu Y (2024). showtext: Using Fonts More Easily in R Graphs. R package version 0.9-7. https://CRAN.R-project.org/package=showtext

Stan Development Team (2024). cmdstanr: R Interface to CmdStan. R package version 0.7.0. https://mc-stan.org/cmdstanr/

Wickham H, et al. (2019). Welcome to the tidyverse. Journal of Open Source Software, 4 (43), 1686. https://doi.org/10.21105/joss.01686

This website reflects the author's personal exploration of ideas and methods. The views expressed are solely their own and may not represent the policies or practices of any affiliated organizations, employers, or clients. Different perspectives, goals, or constraints within teams or organizations can lead to varying appropriate methods. The information provided is for general informational purposes only and should not be construed as legal, actuarial, or professional advice.

{kind=link}